Daily sickness benefits insurance

As an employer, you are obliged to keep paying the salaries of employees who are absent due to illness or pregnancy. Helsana Business Salary assumes this continued payment of salary on your behalf, turning unforeseeable costs into predictable expenses and shielding your employees from loss of earnings.

Benefits for your company

Healthy employees

If you want to improve health in your workplace, our specialists will be happy to help you with modular courses and learning materials on health management.

Budget for prevention services

With a Prevention Budget, you can benefit from an amount earmarked for prevention services – such as Helsana Business Health or Health4Business – within the insurance year. You set the amount yourself. This Prevention Budget also helps you plan measures such as workshops and individual coaching at an early stage to suit your needs.

In the first year of your contract, you will additionally receive a free situation analysis.

Relief of the administration

Whenever you need it, we'll help you with administrative tasks – such as coordination between different public authorities and insurers. Our insurance expertise will enable us to deal with administrative tasks quickly and professionally.

Positioning as an attractive employer

By providing your staff with better cover, you are positioning yourself as the sort of socially responsible employer people will want to work for, and you will show your employees that you appreciate them. You can also enhance your position by giving fathers paternity leave that goes above and beyond the benefits provided by the loss of earnings compensation required by law (EO).

Calculable costs

Helsana Business Salary enables you to turn your financial risk into fixed and calculable costs. We guarantee the uninterrupted continuing payment of wages until the disability pension, or, later, the retirement pension, become payable. By doing that, we take the pressure off your pension fund, too.

Support and reintegration

Getting back to normal living – both at work and socially – following illness is a major challenge. Our Case Managers will try to get in contact with you and the sick employee at an early stage in order to work out together how to reintegrate them into the workplace quickly and successfully.

Insure paternity leave as well

In addition to the maternity benefits for mothers that we already know about, employers can also insure paternity leave for working fathers from 1 January 2022 in addition to the statutory EO paternity insurance. The prerequisite is a daily sickness benefits insurance contract in line with the Federal Insurance Contract Act that also covers maternity benefits. A daily allowance amount of 80%, 90% or 100% of the AHV salary for a benefit duration of 14, 21 or 28 days can also be agreed.

Why is daily sickness allowance insurance worthwhile?

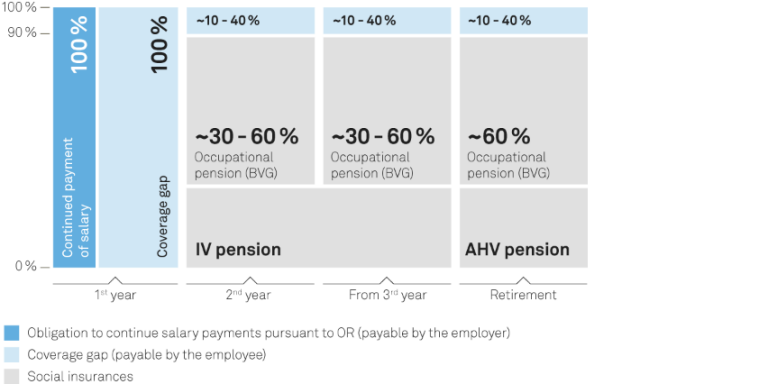

The length of time over which you have to keep on paying a sick employee's wages varies from region to region and depends on the length of time they have been working for you. This presents a financial risk that cannot be calculated for your company, but one you can cover with daily sickness benefits insurance. You pay the premiums, and we handle the continuing wages payments until any benefits from social insurance kick in.

For your employees, the legal provision gives rise to an uncovered risk. The reason for this is that the legally prescribed period for the continuation of salary payments is too short to span the time left until any social insurance pensions (disability or retirement) become payable. You can use daily sickness benefits insurance to bridge this gap in your employees' cover.

Situation without daily sickness benefits insurance

Benefits from last salary in % (AHV salary)

Waiting period, amount and duration of the daily benefits – you use these to adjust the sickness benefits to your own business situation:

Flexible waiting period of between 0 and 360 days

By choosing a waiting period, you decide for yourself for how long you want to keep on paying employees' wages when they fall ill: or, to put it another way, when the insurer should start paying the daily sickness benefits. A longer waiting period reduces the premiums you have to pay.

Daily benefits of between 80% and 100% of the insured salary

A daily benefit of at least 80% exempts you from the legal duty of continuing to pay wages, as it's recognised as being of equivalent value as a solution. A higher daily benefit means you're offering your employees more than the minimum required by law.

Choice of how long the benefits are paid for: 365 or 730 days

The choice of the most suitable benefit duration depends on your occupational pension arrangements (BVG). If you decide that benefits should be paid for 730 days, payment of the occupational pension can be deferred. By doing that, you not only take the pressure off your pension fund and save on risk premiums, but are also putting your employees in a much better position.

Answers to frequently asked questions about daily sickness benefits insurance

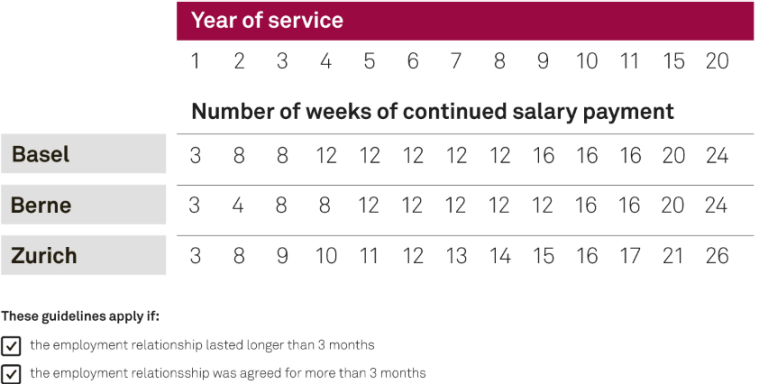

The duration of the continuing salary payments is determined by reference to the number of years in the job and varies from one region to another. The differences are highlighted by the following three scales, known as the Basle, Berne and Zurich scales:

Scales for continuing salary payments

The Helsana Business Salary daily sickness benefits insurance will take over payment of the sick employee's wages after a waiting period that can be chosen according to your individual needs. Employers are obliged by Art. 324b of the Code of Obligations to carry on paying wages in full in this way. If they have recourse to an insurance solution, the amount they are obliged to pay is reduced to 80%, which may be wholly or partly borne by the insurer, depending on how the arrangement is set up.

Daily sickness benefits

The person who is ill receives daily benefits from Helsana. Its amount is calculated on the basis of the insured salary, the degree of incapacity to work and the amount of benefit as agreed. You, the employer, have a free choice as regards the level of benefit. Once it reaches 80%, the law discharges you from any further obligations. If you opt for a lower amount, you remain obliged to top up the insured benefit to reach 80% of the salary.

Example: An employee on a CHF 100,000 salary becomes 50% incapable of work; 80% of his salary is the insured benefit. The daily benefit is CHF 109.60 (80% of 50% of CHF 100,000/365 days).

Benefits are payable for 365 to 730 days, beginning with the day on which the employee becomes incapable of working. However, the payment of the daily benefits does not start until the waiting period is over.

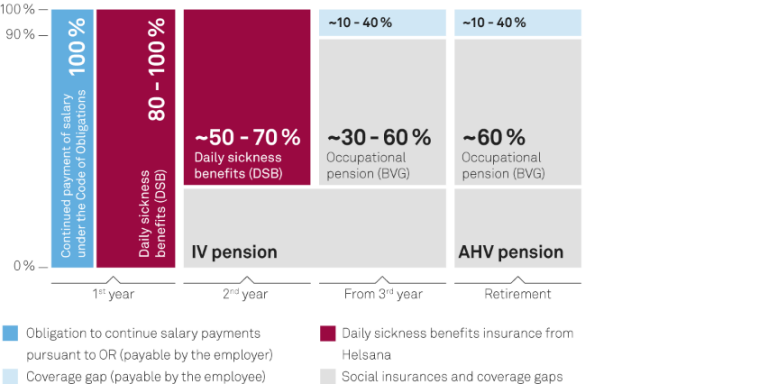

Situation with daily sickness benefits insurance

Benefits from last salary in % (AHV salary)

Continued payment of salary in the event of death

If an employee dies as a result of illness, you as an employer are obliged to continue to pay the salary to surviving relatives for a set period of time. As part of daily sickness benefits insurance, Helsana will support you financially in fulfilling your legal obligation to provide continued payment of salary (in accordance with Art. 338 para. 2 of the Swiss Code of Obligations).

Maternity benefits

For the expectant mothers in your firm, you can also arrange additional benefits over and above what is provided by the maternity insurance required by law: 80% - 100% of the insured person's AHV salary for 14 weeks (VVG, if benefit is greater than 80% ) or 16 weeks (KVG and VVG).

Paternity leave

For the working fathers in your firm, you can also arrange supplementary insurance benefits over and above what is provided by the paternity insurance required by law: 80%, 90% or 100% of the insured person’s AHV salary for a period of 14 (if the benefit is greater than 80%), 21 or 28 days. The prerequisite is that maternity benefits are also covered under a daily sickness benefit insurance contract in line with the Federal Insurance Contract Act.

For self-employed persons: daily benefits following an accident

Are you working for yourself? If you don't have obligatory insurance under the Federal Law on Accident Insurance (UVG), you can insure yourself against the consequences of accidents. You can be covered for up to 100% of your earned income for 365 or 730 days after a waiting period of between 14 and 90 days.

Contact us as soon as an employee reports sick – you can do it online, too. We'll check the claim as soon as it's received. Once the agreed waiting period is over, the daily sickness benefits insurance pays out. Depending on what was agreed when the contract was concluded, the daily sickness benefits is paid out either to the employer or straight to the employees. The person who is ill can require the insurer to pay it out to them directly at any time.

As the policyholder, the employer is liable to pay the premium to the insurer. However, in the case of daily sickness benefits insurance, up to 50% of the premium costs can be passed on to employees, provided that the daily benefit covers at least 80% of their salary.

All daily sickness benefits insurance is voluntary. The insurance allows companies to cover the financial risks associated with the obligation to continue salary payments as defined in Article 324a of the Swiss Code of Obligations.

The company is released from the obligations set out in Article 324a (4) if it takes out insurance to cover at least 80% of the employees' loss of income.

The insurance can be taken out under either the Federal Health Insurance Act (KVG) or the Federal Act on Insurance Contracts (VVG).

The main difference is in the amount of flexibility. The KVG imposes a compulsory scope of benefits, but the insurer is free to adapt the benefits to reflect the client's requirements under a VVG policy.

Collective agreements are used to define the scope of benefits. If the collective agreement permits a VVG insurance policy, the VVG insurance can have exactly the same content as a KVG policy.

The two main factors in reducing absence costs are the waiting period and your employees' health.

Waiting period

Direct absence costs in your company are made up of two elements: the premiums that you pay for daily benefits insurance and the cost of continuing salary payments during the contractual waiting period. The insurance benefits only kick in at the end of the waiting period.

You can reduce your premium costs by opting for a longer waiting period, which increases the amount of continued salary payments made by you. Don't forget that you will be liable for all the costs associated with an emergency during the waiting period. The waiting period can be used to optimise and leverage costs, but you need to consider your company's situation when defining the waiting period. Our advisors and your broker can help you to assess the company's situation and choose a waiting period that is right for you. You can find some advice on how to assess your company's situation here.

Employee health

The second factor is your employees' health: fewer absences mean lower absence costs. So healthy employees are a key factor in keeping the cost of continued salary payments and premiums down. Our health experts will be happy to help you keep your employees healthy.

Extra savings

Helsana offers attractive package discounts in conjunction with our partner, Swiss Life. In addition to saving money, you also benefit from having a one-stop-shop for harmonised insurance solutions: accident, sickness and occupational pensions.

Most SMEs choose the following insurance cover:

- Daily sickness benefits insurance under VVG

- 80% cover for absence from work

- 30-day waiting period

- Duration of benefits 730 days

This combination means that most of your employees have the best possible sickness and/or accident insurance cover, while you and your company benefit from a healthy balance between direct responsibility, insurance benefits and premium costs.

The maximum duration of benefits – 730 days – provides full cover until any disability pension takes effect. The duration also allows you to defer occupational pension insurance benefits (BVG) for a maximum of 24 months, which reduces the burden on your pension fund and saves on BVG risk premiums.

If you opt for the standard 30-day waiting period, then the company is liable for continuing to pay the employee's salary during that time. A shorter waiting period will reduce that cost, but will hike up your premium.

If you are not insured against accidents through your employer (e.g. self-employed persons), you must include accident insurance in your compulsory health insurance. The compulsory health insurance only covers treatment costs such as medical expenses, hospital costs and medication.

If you wish to purchase cover for the loss of income due to an accident, you must include accident cover in your daily sickness benefits insurance. If you want the same scope of benefits as for compulsory accident insurance, including pension benefits, then you need to include accident cover under your daily sickness benefits rather than voluntary accident insurance based on the UVG.

A smart combination: daily sickness benefits insurance and BVG

Daily sickness benefits are the ideal complement to occupational pension insurance (BVG), as the former is generally taken out so as to pay benefits for 730 days. Disability benefits should be payable after 365 days at the most. However, it often turns out that their payment is delayed by enquiries and doesn't start until later. With benefits paid for 730 days, you're ideally covered and not at risk of any gaps in cover.

More information

Do you have questions?

We're here to help.