Accident insurance

If you're an employer, you're obliged to insure your employees against accidents. If employees suffer accidents or occupational illnesses, this can have serious consequences for their everyday life and work. Compulsory accident insurance alleviates these consequences by providing sound basic financial benefits. In addition to compulsory accident insurance, Helsana Business Accident also provides supplementary accident cover. You can add to the statutory benefits as needed.

Benefits for your company

Modular structure

The benefits under compulsory accident insurance are fixed – but, when you complement it with supplementary accident insurance, it is you and you alone who decides which services you want to claim and which risks you want to cover.

Relief of the administration

We deal with administrative tasks, such as enquiries into conditions of eligibility for benefits, quickly and professionally. We also support you in communication with other stakeholder institutions, such as the disability insurance office and thus saving your organisation time and effort.

You are comprehensively insured

You and your employees are comprehensively insured against the consequences of accidents, whether these are medical expenses, lost earnings or permanent incapacity to work.

Prevention cuts costs

As one of the biggest health insurers in Switzerland, we help you with every aspect of health management – from health promotion to absence management.

All-round care

Helsana offers you all-round care of a kind only few other insurers can. We take preventive action and help you with additional benefits if you so request. We also support you and your employees as they return to regular work.

Do I have to take out accident insurance?

All employees working in Switzerland must be insured against accidents. If you are not self-employed or insured by Suva (the Swiss National Accident Insurance Fund), you are required by law to take out compulsory accident insurance for your employees.

Compulsory accident insurance covers your employees against the consequences of an accident that occurs at work, not at work or occupational illness. Supplementary accident insurance enables you to offer your employees protection over and above the obligatory minimum.

|

|

|

|

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

Compulsory

Voluntary

Medical expenses

Doctor's bills and hospital bills

Medical treatment / other benefits in kind

general hospital ward

Other costs covered by insurance

private/semi-private hospital ward

Incapacity for work

Salary during the absence from work

Daily allowance

80 % of the insured income- max. CHF 148,200 - from the third day after the accident date

Additional daily allowance

Any daily allowance supplement up to 100 % of the full salary

Occupational disability

Living expenses in case of disability

Pensions / compensation

80% of the insure income - max. CHF 148,200

Additional pensions/compensation

Any supplements up to 100% of the full salary

Which benefits are insured?

The benefits payable under compulsory accident insurance are laid down by law. They cover medical expenses, a hospital stay in a general ward and 80% of lost earnings (where the salary does not exceed CHF 148,200). Helsana Business Accident offers you options over and above this compulsory accident insurance. These additions can all be adapted to your needs in modular fashion, independently of one another.

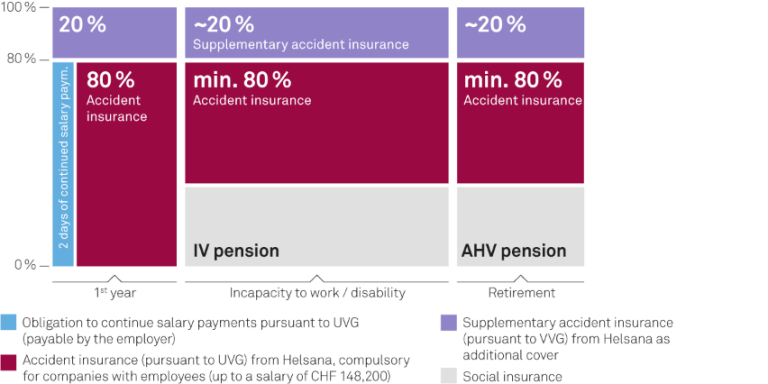

Situation with an accident insurance

Benefits from last salary in %

As an employer, you're obliged to continue to pay at least 80% of an employee's wages from the day of their accident. They become entitled to benefits from compulsory accident insurance from the third day after the accident. That entitlement lapses once the employee is fully recovered and capable of working.

What compulsory accident insurance offers your employees and their family members is financial security after an accident or in the event of disability or even death. It aims to secure their standard of living.

Compulsory accident insurance covers occupational and non-occupational accidents and occupational illnesses.

Occupational accidents are defined as all accidents occurring during working hours. The category also includes accidents sustained before and after work, provided that they are linked with work in some way. It follows that accidents on the way to work are always covered by insurance. Part-time employees working fewer than eight hours a week are covered only in respect of occupational accidents. Accidents sustained by them on the way to work are counted as occupational, while they are non-occupational in the case of all other employees.

Under the UVG, illnesses are treated as occupational in nature if they were brought on in the course of occupational activity mainly or entirely by harmful materials or certain types of work. The insurance also covers illnesses that can be demonstrated to have been brought on solely or very largely by the work done.

Persons insured under obligatory accident insurance are entitled, depending on the circumstances of the individual case, to medical expenses, daily benefits, disability pensions, integrity compensation, helplessness benefits and survivors' pensions.

Medical expenses relate to necessary medical treatment of the consequences of accidents. They also cover the cost of aids to compensate for physical injury, damage to property, and the costs incurred in travel, transportation, rescue, recovery and burial/cremation.

Daily benefits are paid as from the third day after the accident, amounting to no more than 80% of the insured earnings. Insured persons who are completely incapable of working receive the maximum amount. Those who are capable of work to some extent received benefits that are reduced proportionately.

Persons who have become at least 10% disabled as a result of an accident can claim a disability pension. Disability pensions amount to 80% of insured earnings for persons who have become completely incapable of work, and are reduced proportionately where the incapacity is partial.

Anyone whose physical, mental or emotional integrity is substantially and permanently impaired as a result of an accident is entitled to integrity compensation. This compensation takes the form of a one-off payment calculated by reference to the maximum insured earnings and not exceeding it.

A person who has had an accident as a result of which they are disabled and need the help of others to cope with everyday living receives a helplessness benefit. This benefit is paid monthly and is equivalent to at least twice, but no more than six times, the maximum amount they could earn in a day.

On the insured person's death, the surviving family members can claim a survivors' pension. The spouse gets 40%, full orphans 25%, and half-orphans 15% of the insured earnings. All the survivors taken together, though, can receive no more than 70% of the insured earnings in total.

Spouses are entitled to a pension only if they have children who are themselves entitled to one or live with such children in a joint household. In addition, spouses who are at least two-thirds disabled or become so within two years of their spouse's death are entitled to a survivor's pension.

Unlike a widower, a widow is entitled to a pension if she is over 45 years of age or has children who are no longer entitled to a pension. The insurer may, moreover, pay the widow a one-off settlement even if she meets none of the conditions that would entitle her to a pension.

Supplementary accident insurance enables employers like you to add modules to this compulsory accident insurance, and on all three levels: treatment, daily benefits and long-term loss of earnings. The possibilities are many and varied: you can, for example, insure lower wages more generously (100% rather than only 80%) or insure higher salaries above the CHF 148,200 limit imposed by the UVG on insurable earnings. You can also raise the level of accommodation in hospital not only for certain groups of employees but for all of them, from general to semi-private or private.

Medical expenses

After an accident, your employees will benefit from medical treatment, food and accommodation in a hospital’s semi-private (2-bed) or private (single-bed) ward in addition to statutory health insurance and accident insurance. Zudem können sie auch im Spital den Arzt oder die Ärztin frei wählen.

Supplementary accident insurance also covers the costs of certain medications that your employees usually have to pay for themselves as they are not covered by the UVG insurer.

Complementary medicine

Following an accident, Helsana also covers complementary medical treatments when they are considered medically necessary. This means that your employees not only benefit from conventional medicine but also from alternative treatment methods.

Daily benefits

If an employee is certified by a physician to be temporarily incapable of work, Helsana will pay daily benefits of up to 100% of the employee's real salary, starting from the day of the accident, rather than from the third day after it. This will be of particular interest to employees whose salary exceeds the maximum under the UVG of CHF 148,200. Only supplementary insurance will enable these people to have daily benefits sufficient to maintain their accustomed standard of living.

Do your employees need the support of housekeeping services after an accident?

In such cases, Helsana will cover the costs of medically prescribed household help up to a maximum of CHF 5,000 per claim.

Capital insurance

You can insure up to 600% of your employees' real wages. The insured capital will be paid out to them or to their surviving relatives in the event of their disability or death.

Pensions

In the event of disability or death, employees or their surviving relatives receive pensions from compulsory accident insurance, but only up to the maximum salary under the UVG. Supplementary accident insurance calculates these pensions on the basis of their real wages. This helps employees who earn more than the UVG maximum to maintain their standard of living.

Do your employees live in a partnership and have shared children but are not married? Here, Helsana also covers the survivor’s pension and pays this to the surviving partner in the event of death.

Helsana also takes life partners into account in the payout. Additionally, the group of beneficiaries can be individually determined in the event of death. In this case, your employees are not bound by the UVGZ 2023 GIC or the order of inheritance.

Special risks

Where an accident was caused by gross negligence, exceptionally dangerous activities or hazardous behaviour (e.g. taking part in a motocross race), compulsory accident insurance may reduce benefits or refuse outright to pay them. Supplementary accident insurance, on the other hand, can cover these special risks.

Deliberate acts are, however, still excluded. They result in benefits being reduced or withheld in supplementary accident insurance, too.

Cover for costs incurred abroad

Compulsory accident insurance imposes limits on the payment of costs for travel, transport, rescue, the transport of human remains and burial, where these are incurred abroad. It repays no more than twice the amount that the same service would have cost in Switzerland.

Supplementary accident insurance enables you to increase this foreign cover. If you're insured for treatment in a semi-private or private ward, the insurance will cover this when you're abroad too.

As a cross-border commuter, have you fallen off your bike, broken your wrist and are now facing a host of different costs in your country of residence?

No problem. As a cross-border commuter, all your treatment costs in your country of residence are covered, just as they would be for your colleagues treated in Switzerland. In this case, we will cover your excess (in the case of benefits under social insurance) or even any private doctor costs.

Did you break your collarbone on a beach holiday in Cyprus and had to have emergency treatment while there?

No problem. Under your UVGZ contract, the hospital costs of your operation overseas in excess of double the UVG amount are also covered. An emergency operation of this kind in Cyprus can cost CHF 14,000. Double the amount of treatment in Switzerland is around CHF 8,000.

Compulsory accident insurance – payment in instalments

The premiums for compulsory accident insurance are generally paid in advance for the entire financial year. The Accident Insurance Ordinance (UVV), however, allows for the option of paying premiums in half-yearly or quarterly instalments against payment of a surcharge.

Since the last revision of the UVV, the situation regarding interest rates in Switzerland and worldwide has altered considerably. For this reason, the Federal Council decided in June 2022 that the surcharges would be greatly reduced from the beginning of 2023 as part of an amendment to the ordinance. The considerable reduction of the surcharge will relieve the burden on employers who are not able to pay their insurance premiums for the whole year in advance.

The surcharge on instalment payments is currently based on an annual interest rate of 5%. With the amendment to the regulation, it corresponds to an annual interest rate of 1%. At the start of 2023, the surcharge for premium payments in instalments will therefore be 0.25 per cent instead of 1.25 per cent for half-yearly premium payments and 0.375 per cent instead of 1.875 per cent for quarterly premium payments. Helsana will reduce the surcharges on instalment in the same way for supplementary accident insurance.

Answers to frequently asked questions about accident insurance

If an employee becomes incapable of work, you, as an employer, are obliged to continue to pay at least 80% of their wages from the day of their accident. Not until the third day after the accident does compulsory accident insurance take over and start paying daily accident benefits. In the event of permanent incapacity to work, state disability insurance (IV) benefits complement accident insurance payments, if necessary until the day your employee retires. After retirement, the payments in lieu of salary are replaced by the AHV pension.

If the insured person is completely unable to work, they will receive 80% of the insured salary. In cases of partial incapacity for work, the amount is reduced pro rata.

With compulsory accident insurance, the maximum insured annual salary is CHF 148,200. The maximum possible daily benefit is therefore CHF 324.80: 80% of the maximum UVG salary divided by 365.

Supplementary accident insurance can be taken out to cover the salary component that exceeds the CHF 148,200 ceiling.

Your accident insurance and supplementary insurance are valid worldwide.

If you are involved in an accident while abroad, the compulsory insurance will cover up to a maximum of twice the cost of the same benefit in Switzerland. Even better terms apply to EU and EFTA countries.

If you are insured for treatment in a semi-private or private ward, the insurance will cover those costs when you're abroad too.

Whatever happens, if you have an accident while abroad, you are entitled to medical care and treatment until you can be repatriated to Switzerland. All subsequent medical treatment will then be provided in Switzerland.

As the policyholder, the employer is liable to pay the premium to the insurer. For statutory accident insurance, the employer can pass on up to 100% of the non-occupational accident premium to employees. However, this does not apply to occupational accidents, where the employer is liable to pay the full amount.

If the employer takes out supplementary accident insurance cover, the cost of the premiums for accidents at work and outside work can be passed on to employees. Employers usually define the arrangements for passing on insurance costs in the staff regulations.

Employee accident insurance is compulsory and is governed by the Federal Act on Accident Insurance (UVG).

Anyone who is not an employee can include accident cover in their compulsory health insurance. Health insurance with accident cover only insures treatment costs such as medical expenses, hospital costs and medication.

Self-employed persons can take out voluntary accident insurance and have two options to choose from. One option is a daily sickness benefits insurance policy that includes absences from work due to an accident. Alternatively, self-employed persons can voluntarily take out statutory accident insurance (UVG). This solution gives the policyholder the same protection and benefits as an employee.

Under the Federal Act on Accident Insurance (UVG), salaries can be insured up to a maximum of CHF 148,200. This part of the salary is known as the UVG salary. The salary component above the threshold is not insured under compulsory accident insurance. However, you can take out supplementary insurance to cover the remainder (surplus salary).

Two examples:

- The salary of someone who earns CHF 120,000 per annum is fully covered by compulsory accident insurance, because their salary is below the maximum. Daily benefits are calculated based on the salary: 80% of CHF 120,000 = CHF 96,000 (payable in the event of complete incapacity for work).

- Only the first CHF 148,200 is insured for someone who earns CHF 160,000 per year. The daily benefits are calculated using the maximum amount: 80% of CHF 148,200 = CHF 118,560 (payable in the event of complete incapacity for work).

If your employees take out extended insurance, they can continue to benefit from accident insurance cover even after their employment relationship with you has ended. You can find more information here.

More information

Do you have questions?

We're here to help.